Housing Normality

As

soon as we can stabilize housing, all of our troubles will be solved.

This is the mantra we hear night after night on CNBC. The chart below

unmistakably paints an abnormal picture of home prices. Karl

Case, an economics professor at Wellesley College whose name adorns the

S&P Case-Shiller home-price indexes, has studied U.S. house prices

going back to the 1890s. Over the long run, he says, home prices tend

to increase on average at an inflation-adjusted rate of 2.5% to 3% a

year, about the same as per capita income.

![[robert-shiller-graph.png]](http://theburningplatform.com/uploads/image/clip_image005%286%29.jpg)

The

American population has steadily increased from 100 million to 300

million over the last 120 years. Home prices gained at an uneven rate

from 1890 until 2000. Then the combination of bubble boy Alan

Greenspan, Harvard MBA George Bush, delusional home buyers, criminal

investment bankers, pizza delivery boys turned mortgage brokers, and

blind regulators led to the greatest bubble in history. Prices doubled

in many places in six years versus a 15% expected historical return.

Prices have now declined back within the range seen during the period from the 1970s

through the 1990s. This is why the eternal optimists are proclaiming a

housing bottom. These people don�t seem to understand the concept of

averages. An average is created by prices being above average for a

period of time and then below average for a period of time. The current

downturn will over correct to the downside. The most respected housing

expert on the planet, Robert Shiller, recently gave his opinion on the

future of our housing market:

�Even

the federal government has projected price decreases through 2010. As a

baseline, the stress tests recently performed on big banks included a

total fall in housing prices of 41 percent from 2006 through 2010.

Their �more adverse� forecast projected a drop of 48 percent �

suggesting that important housing ratios, like price to rent, and price

to construction cost � would fall to their lowest levels in 20 years. Long

declines do happen with some regularity. And despite the uptick last

week in pending home sales and recent improvement in consumer

confidence, we still appear to be in a continuing price decline. After

the bursting of the Japanese housing bubble in 1991, land prices in

Japan�s major cities fell every single year for 15 consecutive years. Even

if there is a quick end to the recession, the housing market�s poor

performance may linger. After the last home price boom, which ended

about the time of the 1990-91 recession, home prices did not start

moving upward, even incrementally, until 1997.�

![[RIQ12009HomeImprovement.jpg]](http://theburningplatform.com/uploads/image/clip_image008%286%29.jpg)

Residential

investment and home improvement expenditures have averaged 1.07% of GDP

over the last 50 years. This is the 4th time it has peaked above 1.2%.

After the three previous peaks it bottomed below 1%. Based on history,

it will bottom out at .8% in the middle of the next decade. This would

be a reduction of $70 billion in housing investment from the peak.

Great news for Home Depot and Lowes.

A

housing rebound is a virtual impossibility based on any honest

assessment of the facts. Homeowners currently have the least amount of

equity in their homes on record. Real-estate

Web site Zillow.com said that overall, the number of borrowers who are

underwater climbed to 20.4 million at the end of the first quarter from

16.3 million at the end of the fourth quarter. The latest figure

represents 21.9% of all homeowners, according to Zillow, up from 17.6%

in the fourth quarter and 14.3% in the third quarter. There are 75

million homes in the United States. One third of homeowners have no

mortgage, so that means that 41% of all homeowners with a mortgage are

underwater. With prices destined for another 10% to 20% drop, the

number of underwater borrowers will reach 25 million.

MORTGAGE DEBT

There

are over 4 million homes for sale in the U.S. today. This is about one

year�s worth of inventory at current sales levels. You can be sure that

another one million people would love to sell their homes, but haven�t

put their homes on the market. The shills touting their investments on

CNBC every day fail to mention the approaching tsunami of Alt-A

mortgage resets that will get under way in 2010 and not peak until

2013. These Alt-A mortgages are already defaulting at a 20% rate today. There

are $2.4 trillion Alt-A loans outstanding. Alt-A mortgages are

characterized by borrowers with less than full documentation, lower

credit scores, higher loan-to-values, and more investment properties.

There

are more than 2 million Alt-A loans in the U.S. 28 percent of these

loans are held by investors who don�t live in the properties they own.

That includes interest-only home loans and pay-option adjustable rate

mortgages. Option ARMs allow borrowers to pay less than they owe, with

the rest added to the principal of the loan. When the debt exceeds a

pre-set amount, or after a pre- determined time period has passed, the

loan requires a bigger monthly payment.

How can housing return to �normality� with this amount of still toxic debt in the system? It can�t and it won�t.

ALT-A MORTGAGE RESETS

![[mm8.png]](http://theburningplatform.com/uploads/image/clip_image012%288%29.jpg)

Mortgage

delinquencies as a percentage of loans stayed between 2% and 3% from

1979 through 2007. I would categorize this as normal. The Mortgage

Bankers Association just reported a delinquency rate of 9.12% on all

mortgage loans, the highest since the MBA started keeping records in

1972. Also, the delinquency rate only includes late loans (30-days or

more), but not loans in foreclosure. In the first quarter, the

percentage of loans in foreclosure was 3.85%, an increase of 55 basis

points from the prior quarter and 138 basis points from a year ago.

Both the overall percentage and the quarter-to quarter increase are

records. The combined percentage of loans in foreclosure and at least

one payment late is 12.07%, another record. Delinquencies on subprime

mortgage loans rose to 24.95% from 21.88% in the fourth quarter of

2008. Prime loan delinquencies rose to 6.06% from 5.06% one quarter

ago, a significant and disturbing increase from a group of borrowers

that aren�t expected to default.

With

the 30-year mortgage rate approaching 5.7%, mortgage refinancing

activity has plunged about 60% in the last two months. Mortgage

applications for new home purchases collapsed at a 20% annual rate in

May too. Normality in the mortgage market appears to be a few years

away.

MORTGAGE DELINQUENCIES AS A % of LOANS

Household Normality

�You can't drink yourself sober and you can't leverage your way out of excess leverage."

Barry Ritholtz

Barry

is right, but it isn�t stopping the Obama administration from trying to

solve our hangover with a lot more of the dog that bit ya. The current

policy of borrowing in order to stimulate the economy is warped.

Providing more easy credit so poor people can buy Mercedes SUVs will

not solve our problems. The brilliant Doug Casey clearly understands

the policy that should be in effect:

�The

way a society, like an individual, becomes wealthy is by producing more

than it consumes. In other words, by saving, not borrowing. But you

don�t become wealthy by spending and consuming; you become wealthy by

producing and saving. Inflation encourages people to borrow, because

they expect to pay the debt off with cheaper dollars. It encourages

people to mortgage their future. The basic economic fallacy in this is

that a high level of consumption is good. Well, consumption is neither

good nor bad. The problem is the emphasis on consumption financed by

debt -- which leads to the national bankruptcy we�re facing. It�s much

healthier to have an emphasis on production, financed by savings.�

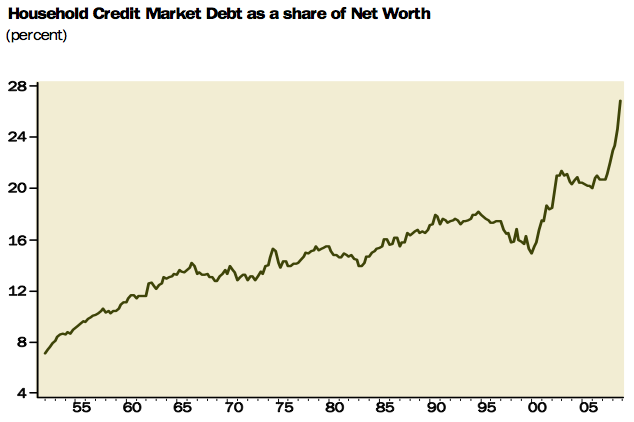

Household

credit market debt currently stands at $13.8 trillion, an all-time

high. It has not fallen. From 1965 through 2000, it ranged from 14% to

17% of Household net worth. It currently stands at 27% of Household net

worth, an all-time high. Is this normal or abnormal? At the end of

2008, household net worth totaled $51.5 trillion, down $11.2 trillion

in one year. In order to get household debt as a percentage of net

worth to a �normal� level of 16%, will require households to either

reduce debt or increase savings by $5.6 trillion. I don�t think this

will be done by next Wednesday. It will take a decade or more.

Source: Haver Analytics, Gluskin Sheff

Famed investor Robert Rodriguez places the blame for our current debt induced collapse squarely at the feet of our government.

�The

regulatory agencies and the federal government were complicit in laying

the groundwork that allowed many of these credit excesses to develop

prior to this economic crisis. Had they done their job effectively, the

economy would not have been pushed to the brink of collapse. I

fundamentally disagree with these �rescue� programs since we believe

our impaired financial system is being distorted by protecting

inefficient and questionable business enterprises. Misguided

measures to re-stimulate consumer borrowing, beyond just getting the

system functioning, are highly questionable. This net worth destruction

is the most severe since the Great Depression. We have a news flash for

the government, creating new credit programs for a consumer who was

spending almost $1.1 trillion more than they were earning in spendable

income, according to MacroMaven�s estimate, will be a non-starter. More

leverage is not what they need. Encouraging the consumer to take on

more debt is like trying to help a recovering heroin addict lessen his

pain by providing him with more heroin.�

If

there is one chart that tells the tale of the U.S. economic demise, it

is the graphic below. It illustrates the transformation of a country

that saved and invested to a country that borrowed and spent. In 1981

consumer expenditures accounted for 62% of GDP and private investment

accounted for 19% of GDP. Consumer expenditures soared to 70% of GDP

while private investment plunged to 11% of GDP. The American economy

needs to revert back to the healthier percentages of 1981. Essentially,

American households need to spend $1 trillion less per year and use

this money to pay down debt and increase savings.

The

Personal Savings rate as a percentage of disposable income dropped

below 0% in 2006. Over the last 50 years, the average has been 7.2%.

The rate has been below this average since 1992. The rate has recently

reached 4% as delusional Boomers are beginning to grasp their bleak

future. Boomers always seem to go too far. They will eventually wear

the badge of frugality as proudly as they wore the badge of

over-consumption. Robert Rodriguez sees an 8% savings rate on the

horizon.

�A

dramatic rise in the U.S. personal savings rate will be required to

begin the mending process of the consumer�s balance sheet. I expect the

U.S. personal savings rate will rise from 2% to 8% this year and remain

at an elevated level for the foreseeable future. This process should

increase savings by approximately $650 billion annually. An increase of

this magnitude, in such a brief period, is unprecedented, other than

during WW2, when it rose from 12% to 24% between 1941 and 1942.

Assuming some earnings on this incremental savings and a partial

recovery in the stock and real-estate markets, it will likely take ten

years for the consumer�s net worth to return to its pre-crisis level.�

Anyone

anticipating a consumer led recovery is counting on consumers who have

been whacked in the head with a 2 by 4 to stagger to their feet and

say, thank you sir may I have another? Even with interest rates at

extremely low levels, household debt service is 14% of disposable

income, versus the 30 year average of 12.1%. As interest rates rise,

this burden will break the consumer�s back. The only way to avoid this

fate is a substantial pay down of debt.

The

only difficulty with paying down debt is you need cash to pay it down.

For decades, from the 1940s until 2000, Americans were cautious about

debt. They always had an emergency fund for those unexpected expenses

that always pop up. If your washer broke, a TV crapped out, or your

lawn mower stopped working you had the cash on hand to buy a new one.

This attitude became pass� as we entered a new century. Who needed cash

when you received three credit card offers per day in the mail? Today,

not only do most Americans not have cash to cover unexpected expenses,

they don�t have cash for milk and bread. A vast swath of America pays

for their cigarettes, lunch meat, and morning coffee with a credit

card. This has resulted in a net $4 trillion deficit of household cash

versus household liabilities. Is this normal or abnormal?

Now

that Americans have used up all the equity in their houses, and some,

they have turned to their last resort � credit cards. The government

has handed billions of taxpayer funds to the biggest credit card

issuers in the world (Bank of America, JP Morgan, Citicorp, Wells

Fargo, Capital One, and American Express) so they will continue to give

grossly overly indebted Americans more rope to hang themselves. This

ridiculous solution will destroy the National balance sheet and the

people who continue to spend more than they make. We are running up the

National credit card balance and passing the bill to future

generations. Credit card delinquencies are already at the highest level

in history. With 25 million (U6 � 16.4%) people unemployed, out of a

work force of 155 million, another 2 to 3 million likely to lose their

jobs, house prices still falling, and foreclosures likely to top 2

million in 2009, credit card delinquencies will surge to unprecedented

levels in 2010. Does anyone really believe our biggest banks are

solvent?

The New Normal

�Loading

up the nation with debt and leaving it for the following generations to

pay is morally irresponsible. To preserve independence, we must not let

our rulers load us with perpetual debt.�

Thomas Jefferson

The

last three decades have not been normal. They�ve been Abby Normal. When

a society chooses to spend more than it produces, the only people who

get rich are the bankers lending out the money. For a society to

progress, its citizens must save more than they spend. The excess

savings can then be utilized to invest in long-term assets that will

increase the wealth of the nation. A society needs to produce more than

it consumes, or it will eventually wither away. Debt keeps Americans

enslaved to the corrupt bankers and clueless government bureaucrats who

run our fair country.

"Debt is an ingenious substitute for the chain and whip of the slave driver."

Ambrose Bierce

When

this debt binge began in 1982, the profits of financial companies

accounted for 7% of all U.S. company profits. At the peak in 2006, they

accounted for more than 30% of all U.S. company profits. This is why

the money managers own the yachts, not the customers. The banking

industry, backed by its sugar daddy the Federal Reserve, has enslaved

the most of America in their web of debt. They have sucked the vitality

and creativity from the nation through the distribution of easy credit.

In the last nine years these whoring bankers went completely mad in

their greed induced search for outrageous levels of compensation by

granting credit to anyone with a breath and creating fraudulent

products to perpetuate ever increasing levels of debt. When this blew

up in their faces these banks should have gone bankrupt and many bank

executives should have gone to jail. Instead, Dr. John Hussman explains

what has happened:

�Rather

than following policies that would have allowed for a sustainable

recovery, our policy makers opted for a stunningly unethical strategy

of making bank bondholders whole with well over a trillion dollars in

public funds, watering down accounting rules to allow banks to go

quietly insolvent while reporting encouraging �operating profits,�

looking beyond the continued shortfall of loan loss reserves in

relation to loan defaults, and doing nothing meaningful with regard to

foreclosures, whose rates continue to soar and which face a fresh wave

later this year and well into 2010 and 2011. These policy responses

have more than doubled the U.S. monetary base within a period of

months, added a trillion more in outstanding Treasury debt, and

virtually assure that the value of those government liabilities will be

re-priced in relation to goods and services over the coming decade. A

range of different methodologies suggest a doubling in U.S. consumer

prices over the coming decade, though with the majority of this

pressure occurring 3-4 years out and beyond.�